Research and Articles

Hotline

- Capital Markets Hotline

- Companies Act Series

- Climate Change Related Legal Issues

- Competition Law Hotline

- Corpsec Hotline

- Court Corner

- Cross Examination

- Deal Destination

- Debt Funding in India Series

- Dispute Resolution Hotline

- Education Sector Hotline

- FEMA Hotline

- Financial Service Update

- Food & Beverages Hotline

- Funds Hotline

- Gaming Law Wrap

- GIFT City Express

- Green Hotline

- HR Law Hotline

- iCe Hotline

- Insolvency and Bankruptcy Hotline

- International Trade Hotlines

- Investment Funds: Monthly Digest

- IP Hotline

- IP Lab

- Legal Update

- Lit Corner

- M&A Disputes Series

- M&A Hotline

- M&A Interactive

- Media Hotline

- New Publication

- Other Hotline

- Pharma & Healthcare Update

- Press Release

- Private Client Wrap

- Private Debt Hotline

- Private Equity Corner

- Real Estate Update

- Realty Check

- Regulatory Digest

- Regulatory Hotline

- Renewable Corner

- SEZ Hotline

- Social Sector Hotline

- Tax Hotline

- Technology & Tax Series

- Technology Law Analysis

- Telecom Hotline

- The Startups Series

- White Collar and Investigations Practice

- Yes, Governance Matters.

- Japan Desk ジャパンデスク

Tax Hotline

June 28, 2025Taxability of One-Time Voluntary Payment Received on Diminution of Value of ESOPs

-

The Hon’ble Karnataka High Court has held that a one-time, voluntary payment by the parent foreign company to ESOP holders in India to compensate for the diminution in the value of their unexercised stock options (both vested and unvested) is a capital receipt.

-

The Karnataka High Court reaffirmed the principle that the taxable event for ESOP perquisites under Section 17(2)(vi) of the Income-tax Act, 1961 is the ‘exercise’ of the option. In the absence of such an event, the statutory computation mechanism fails, and consequently, the charge to tax cannot be sustained for ESOPs as a perquisite.

-

The Karnataka High Court also reaffirmed the principle that in absence of transfer of a ‘capital asset’, such compensation cannot be taxed as ‘capital gains'

-

This ruling aligns with the view previously taken by the Hon’ble Delhi High Court wherein it held such one-time voluntary payment doesn’t qualify as perquisite in absence of exercise of ESOPs held by the employees. However, this ruling and the Delhi High Court ruling is in direct conflict with the decision of the Hon’ble Madras High Court on the same set of facts. holding such payment to be taxable as perquisites.

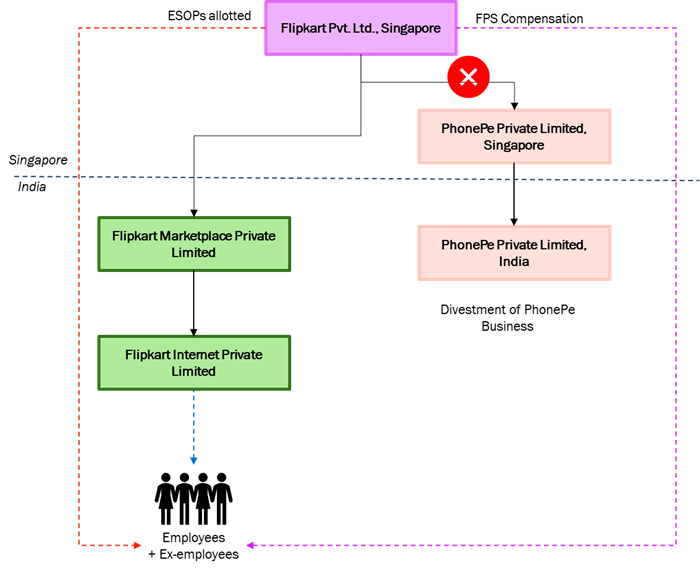

BACKGROUND

The taxability of a one-time compensation (“FPS Compensation”) paid by Flipkart Private Limited, Singapore (“FPS”) to holders of its Employee Stock Options (“ESOPs”) has been a subject of 3 judicial decisions in India. The FPS Compensation was made following the complete separation/divestment of its PhonePe business by FPS in 2022, which led to a diminution in the value of FPS’s shares and, consequently, the value of its ESOPs. Importantly, there was no legal or contractual obligation on FPS to pay any compensation to ESOP holders towards loss in value of ESOPs on account of divestment of PhonePe business. Even after the receipt of FPS Compensation, the ESOP holders continue to retain all ESOPs and the right to receive the same number of shares of FPS subject to vesting and exercise.

The controversy arose pursuant to the denial of ESOP holders’ request for obtaining ‘Nil’ withholding tax certificate under Section 197 of the Income-tax Act, 1961 (“ITA”) in relation to the aforesaid FPS Compensation. The ESOP holders filed a writ petition against the impugned order before their respective jurisdictional High Courts. The core issue revolved around whether the FPS Compensation should be treated as a non-taxable capital receipt or a taxable (i) as perquisite under the head ‘Salaries’ (due to its connection with employment) or (ii) under the head ’Capital Gains’.

The judicial discourse began with the Hon’ble Delhi High Court in case of Sanjay Baweja v. DCIT¹ holding that the FPS Compensation does not qualify as perquisite in absence exercise of ESOPs held by the employees. The Hon’ble Madras High Court, in Nishithkumar Mukeshkumar Mehta v. DCIT², took a divergent view, classifying the payment as a taxable perquisite. In this regard, the Hon’ble Madras High Court held as follows:

-

ESOPs do not qualify as ‘capital assets’3 under section 2(14) of the ITA as they do not fall within the ambit of the expression ‘property of any kind held by an assessee’. ESOPs are rights in relation to ‘capital assets’, i.e. rights to receive ‘capital assets’ (shares) subject to the terms and conditions of the ESOP scheme. Since the taxpayer has no rights in the Indian company of which he is an employee (other than the rights available as an employee), Explanation 1 to Section 2(14) of the ITA is also not attracted.

-

ESOPs are contractual rights that may qualify as actionable claims or choses inaction in certain circumstances. ESOPs are not a source of revenue or profit-making apparatus for the holder because these actionable claims are, intrinsically, not capable of generating revenue (notional or actual) and cannot be monetised, whether by transfer or otherwise, until shares are allotted. Even at the time of allotment, there is notional but not actual benefit. Actual benefit accrues only upon transfer provided there is a capital gain;

-

The FPS Compensation was not towards the loss of or even sterilization of a profit-making apparatus but by way of a discretionary payment towards - potential, as regards unvested options, or actual, as regards vested options - diminution in value of contractual rights;

-

The ESOP scheme did not contain any representation or warranty to ESOP holders that no action would be taken that could impair the value of the ESOPs. Therefore, there was no contractual right to compensation. In the absence of a contractual right to compensation for diminution in value, it cannot be said that a non-existent right was relinquished. The ESOP holder has the right to receive shares upon exercise of the options and the right to claim compensation if such right were to be breached;

-

Considering the above, the receipt was not a capital receipt due to the non-qualification of ESOPs as a ‘capital asset’;

-

The scope of the term ‘specified security’ in Section 17(2)(vi) of the ITA and the phrase ‘value of any specified security’, in the context of ESOPs has to be considered expansively. The term ‘specified security’ is not confined to allotted shares, but also includes securities offered to the holder of ESOPs, and the phrase ‘the value of any specified security’ is wide enough to include a discretionary compensation paid to ESOP holders and can be taxed as ‘perquisites’. Accordingly, the FPS Compensation qualifies as taxable ‘perquisites’.

The Hon’ble Karnataka High Court (“Kar HC”) has now weighed in on the matter in the case of Manjeet Singh Chawla v. DCIT4, aligning with the decision of the Delhi High Court in Sanjay Baweja case and distinguishing the decision of Madras High Court in the Nishithkumar case.

DECISION OF THE KARNATAKA HIGH COURT

The Kar HC, allowing the employee’s writ petition, quashed the order of the Income-tax authorities (“IT Authorities”) which had rejected the application for a ‘Nil’ Tax Deduction Certificate under Section 197 of the ITA. The Kar HC directed the IT Authorities to issue the certificate, holding that the compensation received was not exigible to tax in the hands of the petitioner. In arriving to the aforesaid conclusion, the Kar HC held as follows:

-

No tax deduction on ‘income’ not chargeable to tax: Tax cannot be deducted on payments which do not constitute ‘income’. Further, the power of the IT Authorities to direct tax deduction under Section 197 of the ITA can be exercised only where there is an ‘income’ chargeable to tax

-

The FPS Compensation is a capital receipt: FPS Compensation is a one-time, voluntary compensatory payment (without any corresponding contractual obligation) for the reduction in value of the ESOPs held by the petitioner which is the profit making structure of the petitioner. In arriving at this conclusion, the Kar HC noted that the number of ESOPs held by the petitioner remained same even after the payment of the FPS Compensation.

-

Receipt not chargeable as Capital Gains: Since the ‘cost of acquisition’ of stock options held by the petitioner cannot be determined, the computation mechanism provided for computing capital gains, under Section 48 of the ITA, cannot be applied. Therefore, FPS Compensation, a capital receipt, cannot be taxed as capital gains under Section 45 of the ITA as the charging section and the computation section constitutes an integrated code. In this regard, reliance was placed on the the Hon’ble Supreme Court’s decision in case of B.C. Srinivasa Setty.5

-

The FPS Compensation cannot be treated as salary or perquisite under the ITA: The Kar HC noted that ESOPs have 5 stages: (I) Issuance of options, (II) Vesting of options, (III) Exercise of options, (IV) Issuance of shares, and (V) Sale of such shares. Under the ITA, the Kar HC further noted that ESOPs are taxed at only two stages:

-

Stage III (Exercise of options) - As a ‘perquisite’ under Section 17(2)(vi) of the ITA at the time the ESOP holder exercises the vested option. The taxable value is the difference between the Fair Market Value (FMV) of the shares on the date of exercise and the exercise price paid by the ESOP holder.

-

Stage V (Sale of such shares) - As ‘capital gains’ under Section 45 at the time the shares acquired upon exercise are sold.

-

In the present case, the petitioner had neither exercised the options, nor transferred/ sold any shares. Since the computation of an ‘perquisite’ for ESOPs under Section 17(2)(vi) of the ITA is inextricably linked to actual exercise and allotment of shares, the machinery for computation failed, hence, the FPS Compensation cannot be taxed as ‘perquisites’ under Section 17(2)(vi) of the ITA.

-

Capital receipt not taxable under other heads: The FPS Compensation, being a capital receipt not chargeable under the head ‘Capital Gains’ under Section 45 of the ITA, cannot be brought to tax under any other head of income, including ‘Income from other sources’. In this regard, reliance was placed on the decision of the Hon’ble Supreme Court in case of D.P. Sandu Bros6case wherein it was held that heads of income provided under the ITA are mutually exclusive and where any item of ‘income’ falls specifically under one head, it has to be charged under that head and no other.

The Kar HC didn’t distinguished the Hon’ble Madras High Court decision in the Nishithkumar case on the following grounds:

-

Taxability of the FPS Compensation as salary or perquisite was not in question before the Hon’ble Madras High Court. The only issue under challenge before the Hon’ble Madras High Court was whether impugned order was correct in holding that (i) there was a right to sue which was created in favor of the petitioner, (ii) such right to sue was a ‘capital asset’ which was transferred by the petitioner, (iii) the compensation received could be regarded as consideration for such a transfer, and (iv) this could be taxed under the head 'Capital Gains’.

-

The definition of ‘capital asset’ under Section 2(14) of the ITA is extremely wide and covers ‘property’ of all kinds. The Hon’ble Madras High Court misconstrued Explanation-1 to Section 2(14) of the ITA which clarifies that ‘property’ includes “any rights in, or in relation to an Indian company, including rights of management or control or any other rights whatsoever”. The Madras High Court failed to appreciate that Explanation-1 cannot lead to a conclusion that rights in shares of a foreign company could not be considered a ‘property’ for qualifying as a ‘capital asset’.

-

The Hon’ble Madras High Court erroneously held that (i) ESOPs are not a source of revenue and not capable of generating revenue, and (ii) ESOPs are actionable claim not capable of generating revenue. Further, the Hon’ble Madras High Court ignored the fact that there was a permanent loss of revenue generating source. Such reasoning fails to appreciate that the options held by the petitioner are ‘capital assets’ which are an income earning source, and it is a settled principle of law that the compensation/windfall awarded in lieu of diminishing of profit making structure would be a ‘capital receipt’.

-

The Hon’ble Madras High Court incorrectly invoked section 17(2)(vi) of the ITA. The Kar HC reiterated that taxability under section 17(2)(vi) cannot arise in absence of ‘exercise’ of options by the taxpayer. The Hon’ble Madras High Court incorrectly overlooked the fundamental principle that a tax charge fails if the computation mechanism provided in the statute cannot be applied. Since Section 17(2)(vi) requires the ‘exercise’ of an option to calculate the perquisite value, an event that did not happen in the facts of the petitioner, the FPS Compensation couldn’t be subject to tax as a ‘perquisite’.

-

Section 17(2)(vi) of the ITA provides the value of ‘specified security’ allotted or transferred, directly or indirectly, by an employer or former employer, free of cost or concessional rate to a taxpayer as ‘perquisite’ for taxation under the head ‘Salaries’. Explanation (a) to Section 17(2)(vi) of the ITA provides the scope of the term ‘specified security’ by using the expression “where employees’ stock option has been granted under any plan or scheme therefor, includes the securities offered under such plan or scheme”.

The Hon’ble Madras High Court erroneously concluded that the term ‘specified security’, in the context of ESOPs, is not confined to allotted shares, but includes securities offered to the holder of ESOPs. Further, the Hon’ble Madras High Court erroneously made the consequent finding that the language used in Section 17(2)(vi) of the ITA (i.e., ‘the value of any specified security’) is wide enough to include a discretionary compensation paid to ESOP holders and can be taxed as ‘perquisites’. -

Lastly, the Kar HC made a factual distinction noting that the FPS Compensation was paid not just to employees but to a wider group of option holders, including advisors and consultants. The Kar HC noted that a compensation to such diverse group could not be characterized as ‘perquisite’.

NDA ANALYSIS

ESOPs are a key tool for multinational corporations (MNCs) / startups to attract, motivate, and retain talent across their global operations. By granting ESOPs to employees of all group companies, MNCs aim to foster a sense of ownership and align individual success with the company's overall performance. This is particularly vital in the competitive startup ecosystem, where ESOPs often form a significant part of an employee's total compensation and are often seen as a tool for wealth creation for employees.

Typically, an MNC’s ESOPs are governed by a Global ESOP Plan established at the holding company level. An ESOP Plan inter-alia contains the details of eligible participants, vesting conditions, manner of exercise of shares, good leaver / bad leaver provisions etc. These rulings underscore the critical importance of having meticulous and comprehensive documentation for ESOP terms and conditions. The respective High Courts have thoroughly scrutinized the ESOP documents to determine the characterization of payments made to employees.Having said this, a clear 2:1 split among High Courts on identical facts introduces considerable uncertainty for the future on similar issues. The key point of judicial divergence lies in the interpretation of Section 17(2)(vi) of the ITA.

-

The Hon’ble Delhi Court and Kar HC’s view: This view adopts a strict and literal interpretation of the law. It holds that the statute provides a specific mechanism and a specific event (i.e. exercise of option) for the taxation of ESOPs as perquisites. If that event does not occur, there can be no tax. The payment is therefore assessed based on its intrinsic character – compensation for the partial sterilisation or impairment of a ‘capital asset’ – which makes it a capital receipt.

-

The Hon’ble Madras High Court’s view: This view adopts a more substance-oriented interpretation. It holds that since ESOPs are granted by virtue of employment, any benefit flowing from them, directly or indirectly, partakes the character of a perquisite. The inclusive definitions of ‘salary’ and ‘perquisite’ are broad enough to cover such a payment. The court reasoned that the absence of a specific computation method for an unexercised option should not defeat the charge of tax, especially when the monetary value of the benefit received is clearly known. The court supported this position with the broader principle laid down by SC in Infosys Technologies Ltd.7 case that the “benefit from the ESOP is to be determined for purposes of, and as a prerequisite for, taxation as a ‘perquisite’”.

Another aspect of divergence is in relation to whether ESOPs can qualify as ‘capital assets’ or not. While the Hon’ble Madras High Court interpreted the provisions in relation to perquisite taxation liberally, it took a narrow interpretation of definition of ‘capital asset’ in arriving to the conclusion that ESOPs are not ‘capital assets’. On the other hand, the Kar HC held that the definition of capital assets is extremely wide and covers ‘property’ of any kind. While the determination of whether ESOPs qualify as ‘capital assets’ is important, in this case, the determination may be moot considering that there was no ‘transfer’ of capital asset in the first place by the petitioners.

Having said this, determination of whether ESOPs qualify as ‘capital assets’ or not may be relevant from a transaction perspective. In case of reorganizations / acquisitions at global level, it is not uncommon for companies to cancel / roll-over ESOPs of employees depending upon whether such employees continue their employment or not. In case where employment is terminated, the vested options are cancelled in consideration of payment and unvested options are cancelled without payment of any consideration. While there may be no tax implications on cancellation of unvested options, characterization of payment received pursuant to cancellation of vested options will depend on whether such options are considered as ‘capital assets’ or not. If one were to argue that such options are not capital assets, on basis of strict interpretation of section 17(2)(vi) (as upheld by the Hon’ble Delhi High Court and Hon’ble Kar High Court), there may not be any perquisite taxation in absence of specific exercise by employees.

Further, in case where employment is continued, the options are typically exchanged with options issued by the resulting / acquiring entity. In such cases, determination of whether options qualify as capital asset or not will be crucial. If one were to follow the interpretation by the Hon’ble Madras High Court (i.e. options are not ‘capital assets’), it may be possible to argue that there should not be any tax on exchange of options in absence of exercise by employees.

With three High Courts offering conflicting perspectives, the issue is now ripe for adjudication by the Hon’ble Supreme Court. Until a final verdict is delivered, the tax treatment of payments made pursuant to option plans is likely to remain a litigious issue. Considering that employers have an obligation to withhold tax on salary / perquisite payments, lack of clarity may result in long-drawn litigation and cash flow issues for employees.

Authors

- Shiv Singhal and Ipsita Agarwalla

You can direct your queries or comments to the relevant member.

¹ Sanjay Baweja v. DCIT, [2024] 299 Taxman 313 (Delhi)/[2025] 474 ITR 376 (Delhi)[30-05-2024]. We understand that the Revenue has not filed an appeal against this judgement.

² Nishithkumar Mukeshkumar Mehta v. DCIT, [2024] 165 taxmann.com 386 (Madras)/ [2025] 475 ITR 614 (Madras) [31-07-2024]. The petitioner has filed an appeal before the Divisions Bench of Hon’ble Madras High Court against this judgement vide WA-161845/2024. 3 The term ‘capital asset’ means, inter alia:

“(a) property of any kind held by an assessee, whether or not connected with his business or profession;

…..

Explanation 1.—For the removal of doubts, it is hereby clarified that "property" includes and shall be deemed to have always included any rights in or in relation to an Indian company, including rights of management or control or any other rights whatsoever.”4 Manjeet Singh Chawla v. DCIT. W.P. No. 20212 of 2023 (T-IT) (Karnataka High Court) [02-06-2025]

5 CIT v. B.C. Srinivasa Setty [1981] 128 ITR 294 (SC)

6 CIT vs. D.P. Sandu Bros. Chembur (P.) Ltd., [2005] 142 Taxmann 713 (SC)

7 Commissioner of Income Tax, Bangalore v. Infosys Technologies Ltd., [2008] 297 ITR 167 (SC).

-