Competition Law HotlineFebruary 03, 2025 Gun Jumping Penalty: CCI Denies Availability of Exemption

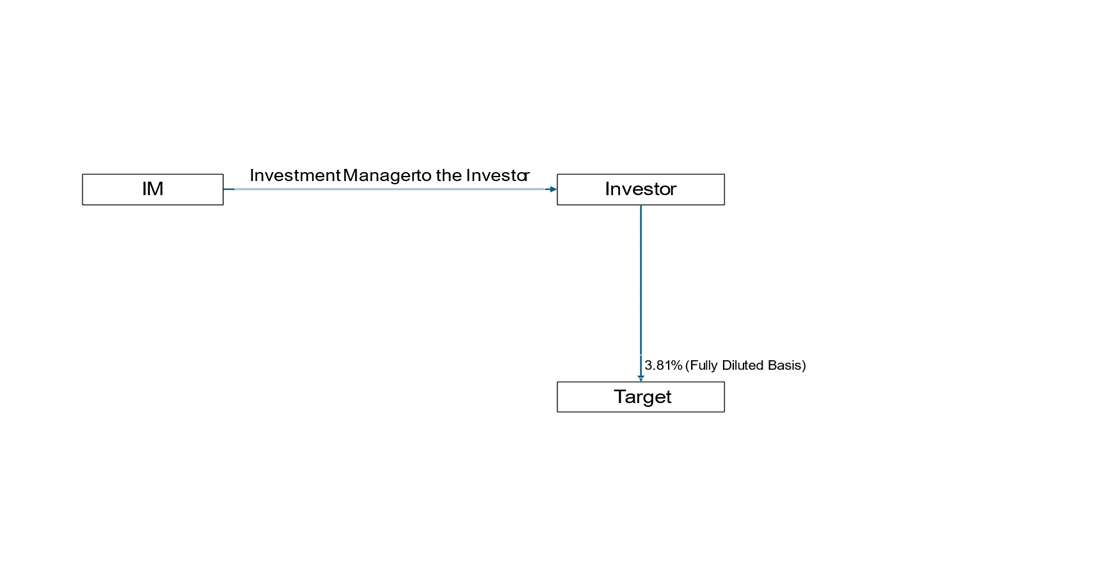

IntroductionThe Competition Commission of India (“CCI” or “Commission”) vide its order (“Order”) dated January 14, 2025, levied a penalty of INR 4,000,000 (Indian Rupees Four Million) collectively on a financial investor (“Investor”) and the Investor’s managing entity (“IM”) (Investor and the IM are collectively referred to as “Acquirer”), under Section 43A of Competition Act, 2002 (the “Act”), for consummating the Transaction (as defined below) without seeking the prior approval of the Commission. The primary objective of the Investor is to engage in investment activities allowed for Category II Alternative Investment Funds as per the SEBI (Alternative Investment Funds) Regulations, 2012. The target is a subsidiary of a listed company in India (“Target”). Brief overview of the transactionThe Investor, acting through its managing entity (IM), subscribed to OCDs issued by the Target by way of entering into a shareholders’ agreement (“SHA”) and securities subscription agreement (“SSA”) (SHA and SSA are collectively referred to as “Transaction Documents”) (“Transaction”). The Transaction was consummated on December 09, 2020 and as on the date of consummation of the Transaction, the Investor held 3.81% shareholding in the Target, on a fully diluted basis.

Figure 1: Transaction Structure

Pursuant to the Transaction Documents, the Investor gained the following key category of rights in relation to the Target. These rights involved,

The Information Rights granted to the Investor under the SHA provided access to (i) certified true copies of minutes of the board, committee, and shareholder meetings, (referred to as “Minutes Rights”), (ii) information about any direct changes in shareholding of the Target and certified true copies of the Target's latest capitalization table. These rights collectively enable the Investor to stay informed and involved in significant aspects of the Target's governance and operations. Key AnalysisThe Transaction was consummated without the prior notification and approval of CCI, which led to the Commission issuing a letter on February 04, 2022 seeking furnishing of information, wherein the Acquirer filed its first response on February 24, 2022 (“First Response”). Pursuant to the First Response, the CCI sought further information vide letter dated June 29, 2022 to which a response and clarification letter was submitted on August 16, 2022 and September 21, 2022, (“Second Response”) respectively (First Response and Second Response collectively referred to as the “Response”). Pursuant to the Response, the Commission issued a show cause notice2 to the Acquirer under Regulation 48 of the CCI (General) Regulations, 2009, read with Section 43A of the Act, asking the Acquirer to show cause for failure to notify the Transaction on the following grounds:

ConclusionBasis the abovementioned reasoning from the Commission, the Commission held that the Acquirer is not entitled to seek the exemption under Item 1 of Schedule I of the Erstwhile Combination Regulations. While, this Order is in furtherance of the Commission’s order in the PI Opportunities Fund34 matter, this Order further affirms the availability of the abovementioned exemptions by stating that only such transactions which (i) are not strategic in nature (i.e.- short-term holding period of investments which are lesser than 10% of shareholding) and (ii) allow the acquirer to exercise rights which are available to ordinary shareholders in a listed company; are considered to be in the ‘ordinary course of business’. Additionally, the availability of the ‘solely as an investment’ exemption under the Competition (Criteria for Exemption of Combinations) Rules, 2024 (“Exemption Rules)5 is also dependent on the acquirer not gaining a right or ability to access ‘commercially sensitive information’. While the term ‘commercially sensitive information’ is not defined in the Exemption Rules and the Act, this Order provides a clarification that Minutes Right shall constitute ‘commercially sensitive information’ and hence, in such cases, the availability of Rule 2 exemption (i.e.- ‘solely as an investment’) under the Schedule to the Exemption Rules may become a challenge.

Authors Gurkeerat Singh, Member, M&A and Private Equity practice Anirudh Arjun, Senior Member, M&A and Private Equity Practice Nishchal Joshipura, Co-Lead, M&A and Private Equity practice

You can direct your queries or comments to the relevant member. 1The AVMs granted to the Acquirer, further involved two categories of AVMs: (i) rights which would be exercised only with the prior written consent of the investor majority, and (ii) rights requiring the prior written consent of all the investors. 2Regulation 48, CCI (General) Regulations, 2009 3Combination Registration Number M&A/Q1/2018/18, dated September 30, 2022 4The Commission in the PI Opportunities Fund matter held that only revenue transactions (i.e.- transactions which are short-term in nature and constitute income and expenditure and are accordingly reflected in the profit and loss account or income statement of the enterprise) are considered to be in the ‘Ordinary Course of Business’. 5Rule1 of the Schedule to Exemption Rules states that “An acquisition of shares of an enterprise in ordinary course of business where the said transaction is-: a) an acquisition of unsubscribed shares upon devolvement as per covenant of an underwriting agreement by any person registered with the Securities and Exchange Board of India established under the Securities and Exchange Board of India Act, 1992 (15 of 1992) or other similar authority established under any law for the time being in force outside India, as an underwriter, in so far as the total shares or voting rights held by the acquirer, directly or indirectly, does not entitle the acquirer to hold more than twenty-five per cent. of the total shares or voting rights of the company, of which shares are being acquired; or b) an acquisition of shares as a stockbroker registered with the Securities and Exchange Board of India, or other similar authority established under any law for the time being in force outside India, in so far as the total shares or voting rights held by the acquirer, directly or indirectly, does not entitle the acquirer to hold more than twenty-five per cent. of the total shares or voting rights of the company, of which shares are being acquired; or c) an acquisition of shares as a mutual fund registered with the Securities and Exchange Board of India, or other similar authority established under any law for the time being in force outside India, in so far as the total shares or voting rights held by the acquirer, directly or indirectly, does not entitle the acquirer to hold more than ten per cent. of the total shares or voting rights of the company, of which shares are being acquired.” DisclaimerThe contents of this hotline should not be construed as legal opinion. View detailed disclaimer. |

|

-

The Competition Commission of India has levied a penalty of INR 4,000,000 (Indian Rupees Four Million) section 43A of the Competition Act, 2002, collectively on a financial investor and it’s managing entity.

-

Access to certified true copies of minutes of shareholders / board / committee; meetings shall enable provision of confidential, commercially sensitive and strategic information.

-

Analysis of the nature and the substance of rights exercisable by the acquirer in relation to the target is critical for determining the availability of the Item 1 exemption under the Schedule I of Competition (Procedure in regard to the transacting of business relating to combinations) Regulations, 2011.

Introduction

The Competition Commission of India (“CCI” or “Commission”) vide its order (“Order”) dated January 14, 2025, levied a penalty of INR 4,000,000 (Indian Rupees Four Million) collectively on a financial investor (“Investor”) and the Investor’s managing entity (“IM”) (Investor and the IM are collectively referred to as “Acquirer”), under Section 43A of Competition Act, 2002 (the “Act”), for consummating the Transaction (as defined below) without seeking the prior approval of the Commission.

The primary objective of the Investor is to engage in investment activities allowed for Category II Alternative Investment Funds as per the SEBI (Alternative Investment Funds) Regulations, 2012. The target is a subsidiary of a listed company in India (“Target”).

Brief overview of the transaction

The Investor, acting through its managing entity (IM), subscribed to OCDs issued by the Target by way of entering into a shareholders’ agreement (“SHA”) and securities subscription agreement (“SSA”) (SHA and SSA are collectively referred to as “Transaction Documents”) (“Transaction”). The Transaction was consummated on December 09, 2020 and as on the date of consummation of the Transaction, the Investor held 3.81% shareholding in the Target, on a fully diluted basis.

Figure 1: Transaction Structure

Pursuant to the Transaction Documents, the Investor gained the following key category of rights in relation to the Target. These rights involved,

-

rights in relation to reserved matters1 (“AVMs”)

-

information rights (“Information Rights”); and

-

inspection rights (“Access Rights”)

The Information Rights granted to the Investor under the SHA provided access to (i) certified true copies of minutes of the board, committee, and shareholder meetings, (referred to as “Minutes Rights”), (ii) information about any direct changes in shareholding of the Target and certified true copies of the Target's latest capitalization table. These rights collectively enable the Investor to stay informed and involved in significant aspects of the Target's governance and operations.

Key Analysis

The Transaction was consummated without the prior notification and approval of CCI, which led to the Commission issuing a letter on February 04, 2022 seeking furnishing of information, wherein the Acquirer filed its first response on February 24, 2022 (“First Response”). Pursuant to the First Response, the CCI sought further information vide letter dated June 29, 2022 to which a response and clarification letter was submitted on August 16, 2022 and September 21, 2022, (“Second Response”) respectively (First Response and Second Response collectively referred to as the “Response”). Pursuant to the Response, the Commission issued a show cause notice2 to the Acquirer under Regulation 48 of the CCI (General) Regulations, 2009, read with Section 43A of the Act, asking the Acquirer to show cause for failure to notify the Transaction on the following grounds:

-

The Transaction allows access to commercially sensitive information

The Minutes Right granted to the Acquirer under the Transaction Documents, allows the Acquirer to access the certified copies of the minutes of the meetings conducted by the board of directors, the shareholders and committees, of the Target. Additionally, the right to access such information is not granted to an ordinary shareholder, since it may permit such shareholder complete access to the strategic and commercially sensitive information of the entity.

While the Acquirer referenced the Commission’s past decisions, arguing that investors with similar rights have not been penalized in the absence of board or observer rights, the Commission highlighted that the Minutes Right and Access Right grants potential access to confidential and commercially sensitive information and strategic information of the Target.

-

The Transaction cannot avail the exemption under Item 1 of Schedule I, Competition (Procedure in regard to the transacting of business relating to combinations) Regulations, 2011 (“Erstwhile Combination Regulations”)

The Acquirer argued that the Transaction would be covered under the conditions laid out for availing the Item 1 exemption under the Erstwhile Combination Regulations, i.e., (i) does not entitle the acquirer to hold more than 25% of the shareholding in the target entity (“Shareholding Condition”), (ii) does not entail the acquisition of control (“Control Condition”), and (iii) the Transaction is solely as an investment (“SIP Condition”) or in the ordinary course of business of the acquirer (“OCB Condition”). Additionally, the Acquirer also argued the severability of the explanation to Item 1 from the exemption itself. While the Commission agreed that the Transaction satisfied the Shareholding Condition and Control Condition, it held that it does not qualify for an exemption under Item 1 since neither the SIP Condition, nor OCB Condition requirements are being met.

SIP Condition: The Acquirer contended that it acquired less than 10% shareholding in the Target (i.e., 3.81% on a fully-diluted basis) without any right to nominate a board member/observer and had no intention to participate in the management or affairs of the Target. Secondly, the Acquirer contended that the Minutes Rights and Access Rights are available to all shareholders of the Target and hence, the abovementioned rights are not available solely to the Acquirer. Additionally, the Acquirer argued that (a) the broader Item 1 exemption is severable from the requirements detailed in the Explanation to Item 1, and (b) the existence of minority investor protection rights cannot affect the availability of the Item 1 exemption.

Firstly, the Commission held that the Item 1 exemption is always applied holistically and is not severable from the Explanation provided thereunder. Secondly, the Commission held that the Acquirer’s interpretation of the Rights Condition is untenable as the abovementioned Minutes Rights and Access Rights go beyond the rights of ordinary shareholders as if any enterprise grants control conferring rights (including the abovementioned Minutes Rights and Access Rights) to all the shareholders of such enterprise, the said rights by virtue of being available to all the shareholders of the enterprise cannot be considered as rights of an ordinary shareholder. The Item 1 provision focuses on assessing transactions where an investor acquires rights that could impact competition or the target's operational dynamics and hence, the Commission viewed that the critical consideration is the nature and substance of the rights.

OCB Condition: The Commission observed that the Acquirer acquired OCDs in 2020 with a final maturity date of January 9, 2026, indicating a significant holding period. Additionally, the Acquirer acquired amongst other rights- AVMs and Information Rights, highlighting that the Transaction was not intended for short-term gains.

The "frequent, routine, and usual" test for ordinary course of business transactions considers not only the execution of transactions but also the investment's intended duration and the investor's role. Ordinary course of business transaction typically involves short-term investments with no rights beyond those of an ordinary shareholder, such as economic and voting rights. Transactions involving longer-term investments and additional rights are not considered as transactions in the ordinary course of business.

-

The Transaction is strategic in nature

The Commission viewed that the Minutes Right and Access Right extend beyond the privileges typically granted to ordinary shareholders, both in their form and substance. Through the Minutes Right, the Acquirer gained exclusive access to commercially sensitive information deliberated during the Target's board meetings. This includes strategic plans, financial data, proprietary technology, business forecasts, and other confidential matters critical to the entities’ competitive advantage and market positioning. In form, such access is not typically afforded to ordinary shareholders, and in substance, it signals that the Acquirer entered into the Transaction from a strategic perspective.

Conclusion

Basis the abovementioned reasoning from the Commission, the Commission held that the Acquirer is not entitled to seek the exemption under Item 1 of Schedule I of the Erstwhile Combination Regulations. While, this Order is in furtherance of the Commission’s order in the PI Opportunities Fund34 matter, this Order further affirms the availability of the abovementioned exemptions by stating that only such transactions which (i) are not strategic in nature (i.e.- short-term holding period of investments which are lesser than 10% of shareholding) and (ii) allow the acquirer to exercise rights which are available to ordinary shareholders in a listed company; are considered to be in the ‘ordinary course of business’.

Additionally, the availability of the ‘solely as an investment’ exemption under the Competition (Criteria for Exemption of Combinations) Rules, 2024 (“Exemption Rules)5 is also dependent on the acquirer not gaining a right or ability to access ‘commercially sensitive information’. While the term ‘commercially sensitive information’ is not defined in the Exemption Rules and the Act, this Order provides a clarification that Minutes Right shall constitute ‘commercially sensitive information’ and hence, in such cases, the availability of Rule 2 exemption (i.e.- ‘solely as an investment’) under the Schedule to the Exemption Rules may become a challenge.

Authors

Gurkeerat Singh, Member, M&A and Private Equity practice

Anirudh Arjun, Senior Member, M&A and Private Equity Practice

Nishchal Joshipura, Co-Lead, M&A and Private Equity practice

You can direct your queries or comments to the relevant member.

1The AVMs granted to the Acquirer, further involved two categories of AVMs: (i) rights which would be exercised only with the prior written consent of the investor majority, and (ii) rights requiring the prior written consent of all the investors.

2Regulation 48, CCI (General) Regulations, 2009

3Combination Registration Number M&A/Q1/2018/18, dated September 30, 2022

4The Commission in the PI Opportunities Fund matter held that only revenue transactions (i.e.- transactions which are short-term in nature and constitute income and expenditure and are accordingly reflected in the profit and loss account or income statement of the enterprise) are considered to be in the ‘Ordinary Course of Business’.

5Rule1 of the Schedule to Exemption Rules states that “An acquisition of shares of an enterprise in ordinary course of business where the said transaction is-:

a) an acquisition of unsubscribed shares upon devolvement as per covenant of an underwriting agreement by any person registered with the Securities and Exchange Board of India established under the Securities and Exchange Board of India Act, 1992 (15 of 1992) or other similar authority established under any law for the time being in force outside India, as an underwriter, in so far as the total shares or voting rights held by the acquirer, directly or indirectly, does not entitle the acquirer to hold more than twenty-five per cent. of the total shares or voting rights of the company, of which shares are being acquired; or

b) an acquisition of shares as a stockbroker registered with the Securities and Exchange Board of India, or other similar authority established under any law for the time being in force outside India, in so far as the total shares or voting rights held by the acquirer, directly or indirectly, does not entitle the acquirer to hold more than twenty-five per cent. of the total shares or voting rights of the company, of which shares are being acquired; or

c) an acquisition of shares as a mutual fund registered with the Securities and Exchange Board of India, or other similar authority established under any law for the time being in force outside India, in so far as the total shares or voting rights held by the acquirer, directly or indirectly, does not entitle the acquirer to hold more than ten per cent. of the total shares or voting rights of the company, of which shares are being acquired.”

Disclaimer

The contents of this hotline should not be construed as legal opinion. View detailed disclaimer.

Research PapersMergers & Acquisitions New Age of Franchising Life Sciences 2025 |

Research Articles |

AudioCCI’s Deal Value Test Securities Market Regulator’s Continued Quest Against “Unfiltered” Financial Advice Digital Lending - Part 1 - What's New with NBFC P2Ps |

NDA ConnectConnect with us at events, |

NDA Hotline |